VANCOUVER, BRITISH COLUMBIA – March 21, 2016

Sands & Associates, BC’s largest firm of Credit Counsellors and Licensed Insolvency Trustees released results of their fourth annual BC Consumer Debt Study today. The 2016 BC Consumer Debt Study provides an in-depth look at consumers’ debt levels, the factors causing individuals’ financial difficulties, with some additional insights into recent trends such as lower mainland housing costs, payday loans and senior citizens’ debt levels.

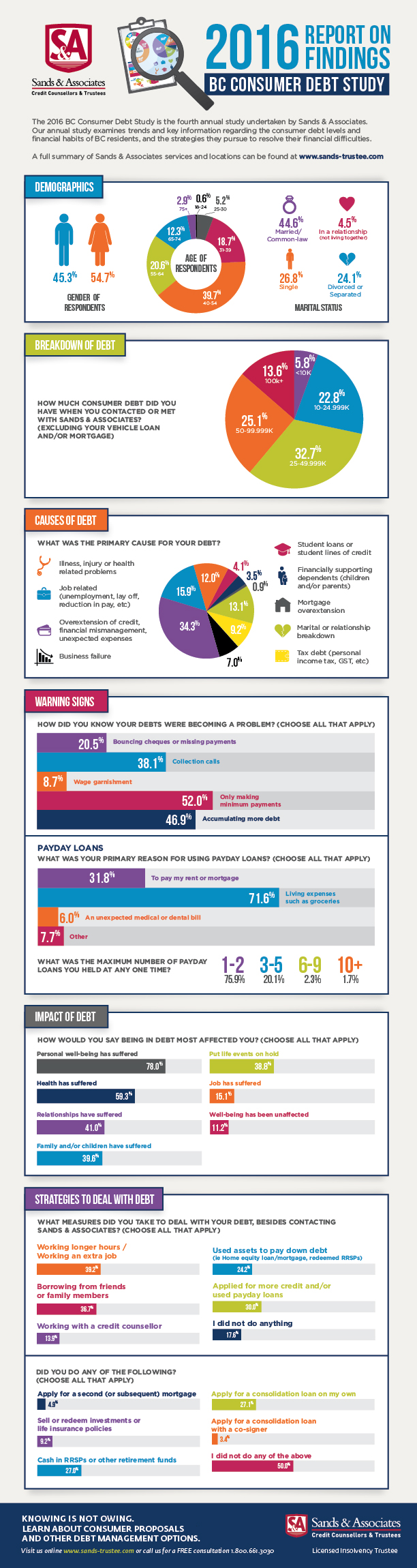

The 2016 BC Consumer Debt study by Sands & Associates is the only BC-specific study to gather and analyze responses from over 1,000 individuals throughout the province to take a closer look at the financial challenges faced and the subsequent strategies adopted by British Columbians.

As financial challenges vary significantly across generations, certain sections of the study are segmented into specific demographics across three different age ranges. Study participants included debtors aged 30 and under (“Youth Generation”); debtors between the ages of 31 and 54 (“Mid-Life/Sandwich Generation”); and debtors aged 55 and older (“Pre-Retirement and Retirement Generation”).

Click here to read the full report in PDF format.

The 2016 BC Consumer Debt Study highlighted the following trends:

- The largest proportion of survey respondents (32.7%) indicated they were carrying between $25,000 to $49,999 worth of unsecured debt (excluding vehicle loans and mortgages) at the time they sought assistance for their debts.

- Overextension of credit, financial mismanagement or unexpected expenses was the top cause of debt as cited by all three generational demographics.

- 52% of respondents indicated that making only minimum payments on debts was the warning sign that made them realize their debts were becoming a problem.

- Nearly one third (30%) of respondents had used payday loans, with the primary reason for using payday loans being to pay day to day living expenses such as groceries (71.6%).

- A large proportion of the Youth Generation (53.3%) and Mid-Life/Sandwich Generation (41.4%) borrowed from friends or family members in attempt to try to deal with their debts.

- 3% of the Pre-Retirement and Retirement Generation cashed in RRSPs or other retirement funds in attempt to resolve their financial situation.

Vice-President of Sands & Associates, Blair Mantin, further adds, “We continue to see seniors with high levels of consumer debts. One of the most concerning aspects of this is how many people needlessly deplete their retirement funds during, or as they approach retirement to try to pay down their debts. They are completely unaware that there are rules in place to protect RRSP funds – and for good reason. Once those funds are gone, there’s generally no way to reestablish retirement savings that those people will so desperately need again down the road.”

Mantin strongly suggests that individuals carrying debts that they cannot pay off in the coming 12-18 months evaluate their financial options with a reputable professional at the onset of concerns. “Over seventy five percent of our survey respondents indicated that they would have taken action sooner if they had been aware of how the processes really work. Licensed Insolvency Trustees are always available to provide information about people’s options – for free.”

Click here to read the full report in PDF format.

About Sands & Associates:

Celebrating over 29 years providing debt solutions, Sands & Associates is British Columbia’s largest firm of Credit Counsellors, Proposal Administrators and Licensed Insolvency Trustees, focused exclusively on personal and small business insolvency services. Now operating from a network of local offices throughout British Columbia, Sands & Associates uses a non-judgmental, empathetic approach to helping resolve financial difficulties and has been recognized as a multi-year Consumer Choice Award winner.